What Is A Federal Student Loan and How Do They Work

Federal student loans are the most common type of loans that students borrow to finance their education. Federal student loans should be the first option used for undergraduate, graduate and professional degrees such as medical school. They come in a variety of loan types, repayment plans, and loan forgiveness options. Most federal student loans are issued at a fixed interest rate. Some older loans, such as Family Federal Education Loans (FFEL), were sometimes issued as variable rate loans.

Here’s what you should know about federal student loans.

Table of Contents

- Subsidized vs. unsubsidized federal student loans

- Types of federal student loans

- Comparing federal student loans

- Health resources and services administration loans

- How to apply for a federal student loan

- What are federal student loan interest rates?

- How to choose which federal student loan?

- Federal student loan repayment programs

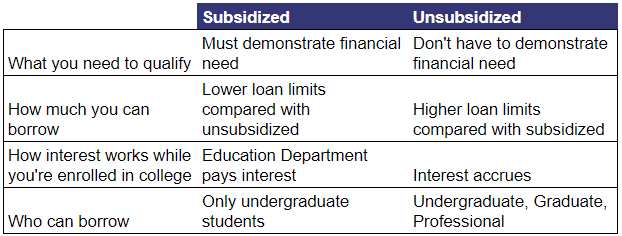

Subsidized vs. Unsubsidized Federal Student Loans

Federal student loans are offered in two main categories: subsidized and unsubsidized. In short, the difference between subsidized and unsubsidized is that direct subsidized loans have slightly better terms, such as lower interest rates, and that interest doesn’t accrue while in school. Since 2012, subsidized federal loans are only offered at the undergraduate level. Anyone pursuing a grad school degree may only utilize unsubsidized loans.

Types of Federal Student Loans

There are five main types of federal student loans to consider.

Direct Stafford Loans

Stafford Loans originated from the William D. Ford Federal Direct Loan (Direct Loan) Program. Direct Stafford Loans are the most common student loans and are currently being issued to help cover the cost of higher education.

There are 3 categories of Stafford Loans:

- Direct Subsidized: Available to undergraduates

- Direct Unsubsidized: Available to undergraduates and graduate students

- Direct Consolidation: Available to undergraduates and graduate students

Prior to consolidation, Stafford Loans are eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

- All Income-Driven Repayment Plans (and Pay As You Earn (PAYE) if borrowed after October 1, 2007 and have a federal loan disbursed on or after October 1, 2011)

- Public Service Loan Forgiveness (PSLF)

- Taxable Income-Driven Repayment Forgiveness

Grad PLUS Loans

Grad PLUS Loans, also known as Graduate PLUS Loans, come from the Direct and Family Federal Education Loan (FFELP) Programs. Borrowers are issued these loans to cover tuition after exhausting Stafford Loans.

Prior to consolidation, Direct Grad PLUS Loans are eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

- All Income-Driven Repayment Plans (and PAYE if borrowed after October 1, 2007 and have a federal loan disbursed on or after October 1, 2011)

- PSLF

- Taxable Income-Driven Repayment Forgiveness

Prior to consolidation, FFEL PLUS Loans are eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

- Income-Based Repayment (IBR)

- Taxable Income-Driven Repayment Forgiveness via IBR

After consolidation, FFEL Grad PLUS Loans are eligible for:

- The remaining Income-Driven Repayment Plans: Revised Pay As You Earn (REPAYE), Income-Contingent Repayment (ICR), and PAYE (if borrowed after October 1, 2007 and have a federal loan disbursed on or after October 1, 2011)

- PSLF

- Taxable Income-Driven Repayment Forgiveness via REPAYE, ICR, PAYE

Parent PLUS Loans

Parent PLUS Loans are issued to parents to finance their child’s education. They are offered for undergraduate, graduate, and professional degree students. Parents will usually take these loans if their child is unable to cover their tuition through federal student loans. Parents are liable for the loans and ultimately responsible for them.

Prior to consolidation, Parent PLUS Loans are only eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

After consolidation, Parent PLUS Loans are eligible for:

- ICR

- Taxable Income-Driven Repayment Forgiveness via ICR

- PSLF

To be eligible for additional IDR plans, you will need to do another consolidation. This type of double consolidation needs careful review and is difficult to get right. We suggest booking a consultation with one of our experts.

Family Federal Education Loan (FFELP) Program

Before 2010, the Family Federal Education Loan (FFELP) Program was the main source of federal student loans. The program ended in 2010. Almost all federal loans are now issued under the Direct Loan program referred to above. But for those who still have these older loans, the following rules apply.

Prior to consolidation, FFELP Loans are eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

- IBR (not to be confused with IDR)

- Taxable Income-Driven Repayment Forgiveness via IBR

After consolidation, FFELP Loans are eligible for:

- The remaining Income-Driven Repayment Plans

- REPAYE, ICR (and PAYE if borrowed after October 1, 2007 and have a federal loan disbursed on or after October 1, 2011)

- PSLF

- Taxable Income-Driven Repayment Forgiveness via REPAYE, ICR, PAYE

Perkins Loans

The Federal Perkins Student Loan Program was created to provide money for college students with lower income or exceptional financial need. The program ended on September 30, 2017.

Perkins Loans all have a 5% interest rate, and they are issued by the school you attend. They are subsidized and won’t accrue interest while enrolled in school.

Perkins Loans aren’t eligible for a number of federal programs, like Income-Driven repayment (IDR) or public service loan forgiveness (PSLF), until they are consolidated.

After consolidation, Perkins loans are eligible for:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

- All Income-Driven Repayment Plans (and PAYE if borrowed after October 1, 2007 and have a federal loan disbursed on or after October 1, 2011)

- PSLF

- Taxable Income-Driven Repayment Forgiveness

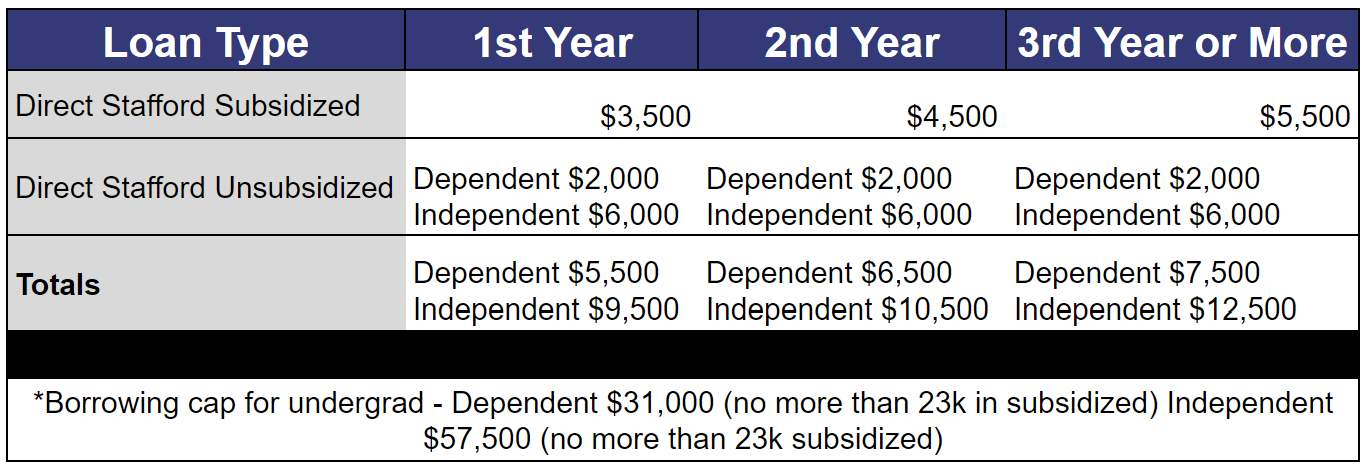

Comparing Federal Student Loans

When you are deciding which federal loans to choose, you don’t have much discretion on which types of loans you will receive. You will obtain a loan offer from Federal Student Aid after you fill out the FASFA form provided by your school’s financial aid office. At the undergraduate level, you’ll receive Direct Stafford subsidized and unsubsidized loans. There’s a cap on how much you can borrow in undergrad federally, and if you need more loans, you’ll have to receive Parent Plus Loans or likely apply for private student loans. More on borrowing thresholds later.

For graduate and professional degree programs, the loans will consist of Direct Stafford unsubsidized loans and Direct Plus Graduate Loans. Direct Plus Graduate Loans are always issued at a 1% higher interest rate than Direct Stafford unsubsidized loans. There is no cap on how much you can borrow federally.

Family Federal Education Loans (FFELP) and Perkins Loans were older-loan types that were discontinued in 2010 and 2017, respectively. These loans tend to have less repayment plans and loan forgiveness options than direct loans (Direct Stafford unsubsidized/subsidized and Direct Plus Graduate).

Each loan type has different rules for repayment and loan forgiveness.

See the below chart to understand more of the nuances for each loan type.

See our repayment or consolidation guides if you’d like to learn more about those topics.

Health Resources and Services Administration Loans

Aside from the most common federal student loans listed above, the Health Resources and Services Administration (HRSA) also issues student loans exclusively to US healthcare professionals who demonstrate a financial need pursuing their healthcare education. HRSA loans are need-based, and they come with service requirements which encourage borrowers to practice in underserved communities. All of these loans are subsidized (government pays interest during school) and have a 5% fixed interest rate. Each has its own repayment terms, forgiveness, and deferment eligibility.

Loans for Disadvantaged Students (LDS)

Must pursue education as a physician, dentist, optometrist, podiatrist, pharmacist or veterinarian. These loans can be deferred during residencies and internships. The repayment term is 10 years, and the debt can become eligible for loan forgiveness through consolidation.

Primary Care Loan

Must pursue an MD or DO program to be eligible and work in primary care. If the borrower does not work in primary care, they will be placed in service default and receive penalty interest on the loans. These loans are not eligible to be consolidated to qualify for loan forgiveness.

Health Professions Student Loan

These loans were discontinued in 1993 and now fall under the Primary Care Loan Program.

How to Apply for a Federal Student Loan

Your school’s website or financial aid office will direct you to the federal student aid form or FAFSA form to receive student loans. After filling out the form, federal student aid will provide you with details on your financial aid package.

Prior to receiving federal student loans, you’ll complete entrance counseling and sign a legal document called a master promissory note in which you promise to agree to the loan obligations. If you have additional questions, contact your school’s financial aid office.

What Are Federal Student Loan Interest Rates?

Federal student loan interest rates follow interest rates set by the Federal Reserve. Each year, they typically change as interest rates fluctuate.

Interest Rates for Direct Student Loans July 1, 2022 to June 30, 2023

What Are Federal Student Loan Fees?

When you take out a federal loan, there is a fee charged. The loan fee comes out of the money paid to you while you’re still in school. So, the money you receive will be less than the amount you actually borrow.

Loan Fees for Direct Student Loans October 1, 2020 to September 31, 2023

Example: Undergraduate borrower needs $5,000. They are issued a loan of $5,287. $5,000 is the actual amount which hits their bank account, but they owe $5,287. $287 is the loan fee. $5,000 * 1.057% = $5,287

How Is the Interest Calculated on Federal Student Loans?

Interest on federal student loans accrues daily, and it is calculated as simple interest. (Loan principal balance * interest rate) * numbers of days since last payment.

Does Interest Capitalize or Compound on Federal Student Loans?

Yes, interest can capitalize, and most of the time it is unavoidable. Interest capitalization is when interest that has accumulated on your loans will become principal, and your loans will start growing off a higher principal balance. More on interest capitalization.

How to Choose Which Federal Student Loan?

When you borrow federally, you choose how much you need, but are not able to select which loan type. The loan type offered depends on how much you borrow and if it’s for undergraduate or graduate/professional school.

Undergraduate Programs

For undergraduate loans, there is a cap on how much you can borrow. Also, your borrowing cap depends on whether you’re a dependent or independent student. Dependent students are assumed to have the support of parents. Independent students are at least 24 years old, married, in graduate/professional school, in the armed forces, have children, etc. Basically, if your parents are going to help you pay for school, you are dependent. If you’re on your own paying for college, you’re independent.

Example: If you are an independent student in your first year and you borrow $5,000, the first $3,500 will be subsidized and the remaining $1,500 will be unsubsidized. You are automatically first issued subsidized loans in undergrad.

If you need more than what’s offered federally, you can look into Parent Plus Loans or Private Student Loans.

Graduate/Professional Degree Programs Non-Healthcare

The current cap for Direct Stafford unsubsidized is $20,500 per year. If you need additional loans for the year, the remainder of your loans will be a Direct Plus Graduate Loan. For example, you need $40,000 to pay for dental school tuition and afford to live. That means $20,500 would be issued as a Direct Stafford Unsubsidized Loan, and the remaining $19,500 would be a Graduate Plus Loan. Direct Stafford Subsidized Loans were discontinued in 2012.

Graduate Professional Programs Medical, Dental or other health professions

Those in graduate health programs have a higher borrowing threshold with Stafford loans, $20,500-$40,500. This will benefit the borrower because they will be able to take out more Direct Stafford Loans before they hit Direct Plus Graduate. Direct Plus Graduate are always issued 1% higher than Direct Stafford Loans.

Federal Student Loan Repayment Programs

There are a number of federal repayment plans to consider when determining which repayment plan is best for you. Standard, Graduated, and Extended repayment are based on your loan amount, length of repayment, and interest rate. Income-Driven Repayment is based on your income and household size.

Before you begin borrowing for school, take time to make a plan on how to pay for it. First, apply for scholarships, grants and look for employment opportunities to reduce the cost of college. After reading this guide, if you’re still not sure on the best route, schedule a pre-debt consult.

Are you ready to tackle your student loans?

Join our community of doctors, dentists and high earners. Each month you’ll get our FREE newsletter with all the tips and tricks to help you save $$ on your student loans.