Federal Student Loan Repayment Calculator

*This calculator is assuming the borrower is single or filing taxes as a couple married filing jointly. If you’d like to run the numbers as a couple married filing separately here’s our resource or hire one of our student loan pros to help you run the numbers

Want to download the calculator? Fill out the below and you’ll receive a link to the calculator and subscription to our monthly newsletter.

How to Estimate Student Loan Repayment

If you’re the DIY type and want to calculate the monthly payment with pen and paper or through a spreadsheet, here’s what you need to know. Discretionary income (DI) is used to calculate your monthly payment in the various IDR plans.

- Standard Repayment Plan – fixed payments over 10 years

- Graduated Repayment Plan – payments start at a lower amount and increase every two years at a rate to pay off the loan over 10 years

- Extended Repayment Plan – fixed payments over 25 years

- Extended Graduated Repayment Plan – payments start at a lower amount and increase every two years at a rate to pay off the loan over 25 years

- Income-Driven Repayment (IDR) Plans – payments are calculated as a percentage of discretionary income. IDR plans are a requirement for Public Service Loan Forgiveness (PSLF).

Standard repayment plan

To calculate monthly payments in the standard repayment plan is quite simple: plug the numbers into a mortgage calculator online or on the calculator on this page.

Inputs

- Interest rate = 7%

- Loan Term = 10 years

- Present Value (loan balance) = $200,000

Here’s the formula

=PMT(7%/12,10*12,200000,0,0) = $2,322

Graduated repayment plan

Calculating monthly payments in the graduated repayment plan is harder than for the standard or extended options. Payments will usually start out about ½ of what payments are in the standard 10-year repayment plan. Every two years, payments will increase. At the end of repayment, payments could be 1.5x what payments are in the standard 10-year repayment plan.

Monthly payments based on the example above would be ~$1,166.

Extended repayment plan

To calculate monthly payments in the extended repayment plan, you follow the same process you do with the standard repayment plan for everything except the term:

Inputs

- Interest rate = 7%

- Loan Term = 25 years

- Present Value (loan balance) = $200,000

Here’s the formula

=PMT(7%/12,25*12,200000,0,0) = $1,413

Income Driven Repayment Plans

IDR plans are calculated differently than the three repayment plans discussed earlier. Payments are based on your income and household size. Your monthly payment is calculated by taking your income and subtracting it by the poverty guideline based on your household size. This gives you discretionary income. Then, based on the IDR plan you pick, it will take 10%-20% of your discretionary income to calculate your monthly payment.

SAVE (formerly REPAYE) =Discretionary Income = AGI minus 225% of the poverty guideline

PAYE, IBR – Discretionary Income = Adjusted Gross Income (AGI) minus 150% of the poverty guideline (based on your family size and state of residence)

ICR – Discretionary Income = AGI minus 100% of the poverty guideline

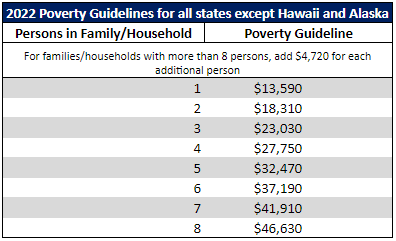

The Department of Health and Human Services (HHS) sets the poverty guidelines. All states except Alaska and Hawaii follow the same poverty guideline which is based on your household size. Your household size is determined by how many children are in your home, including any unborn child who will be born during the year. Children must receive half of their support from you to be claimed.

Here are a couple of examples to illustrate how repayment plans can change your payment

Household size of 2 enrolled in SAVE with income of $200,000; owes $350,000 @ 7% in student loans

- 225% of poverty guideline household of two: 18,310 * 225% = $41,197

- Discretionary Income = $200,000 (income) – $41,197 (poverty guideline) = $158,803

- Monthly Payment in SAVE = 158,803 *10%/12 = $1,323

Household size of 2 enrolled in Old IBR with income of $200,000; owes $350,000 @ 7% in student loans

- 150% of poverty guideline household of two:18,310 *150% = $27,465

- Discretionary Income = $200,000 (income) – $27,465 (poverty guideline) = $172,535

- Monthly Payment in Old IBR = 172,535 *15%/12 = $2,157

Household size of 2 enrolled in ICR with income of $200,000; owes $350,000 @ 7% in student loans

- 100% of poverty guideline household of two:18,310 *100% = $18,310

- Discretionary Income = $200,000 (income) – $18,310 (poverty guideline) = $181,690

- Monthly Payment in ICR = 181,690 *20%/12 = $3,028

Repayment plan selection can be one of the most daunting tasks when you’re determining how to best pay down your loan. Here’s our guide on repayment plans.

How Can You Lower Your Student Loan Payment?

For federal student loans, there are a few different approaches to lower your monthly student loan payment.

-Enroll in an Income-Driven Repayment (IDR) plan instead of the standard 10-year graduated or extended repayment plan.

–Private refinance your federal student loans into a lower interest rate. Typically, this should provide you with a lower payment.

Methods to Reduce Monthly Payments in Income-Driven Repayment Plans

If you are already enrolled in an IDR plan and still would like to reduce your monthly payment, consider these two strategies.

-Contribute to pre-tax accounts, such as 401(k)s, 403(b)s, 457s, TSPs, Health Saving Accounts (HSAs), and Flexible Spending Accounts (FSAs).

-File taxes as a married couple married filing separately (MFS) – learn more about this strategy here.

Sitting down and crunching the numbers can be an eye-opening process. I know it was for me when I was determining how to pay down our loans. Simulate your monthly payments as soon as you know how much you’ll be borrowing for your program to help you identify what monthly payments will be. If you’re done with school, you should have done this yesterday, but today is a good time to start. Having clarity on your payments can help you focus on the task at hand whether you’re a student or busy working professional. If you’re struggling about which repayment plan you should pick or confused with how to begin, schedule a time with one of our pros.